Luxury construction runs on scarcity, and America just noticed a material it forgot it knew. Interest in rammed earth has been climbing for a decade — carbon math, wildfire resilience and a hunger for the singular are all pushing the same direction.

Request a Consultation Call (307) 217-5491Every luxury market eventually exhausts its materials. Marble arrived in every foyer; reclaimed timber got a subscription box; architectural concrete became the default of every boutique hotel lobby between here and Copenhagen. What's left, when everything is available, is the thing that can't be shipped: architecture made from the site itself.

That's the engine underneath rammed earth's American resurgence. The material never went away — Tucson kept the flame through the late twentieth century, and Australia and Europe industrialized the craft — but three forces are now converging on it at once.

Cement is roughly 8% of global emissions, and serious clients now audit embodied carbon the way they audit finances. A stabilized earth wall carries a fraction of concrete's footprint; an unstabilized one approaches zero. For family offices and brands with published commitments, the envelope is suddenly a statement of accounts.

A decade of catastrophic wildfire seasons rewrote how the West thinks about envelopes. Mineral walls don't burn, and insurers have noticed. What used to be an aesthetic conversation now opens with underwriting.

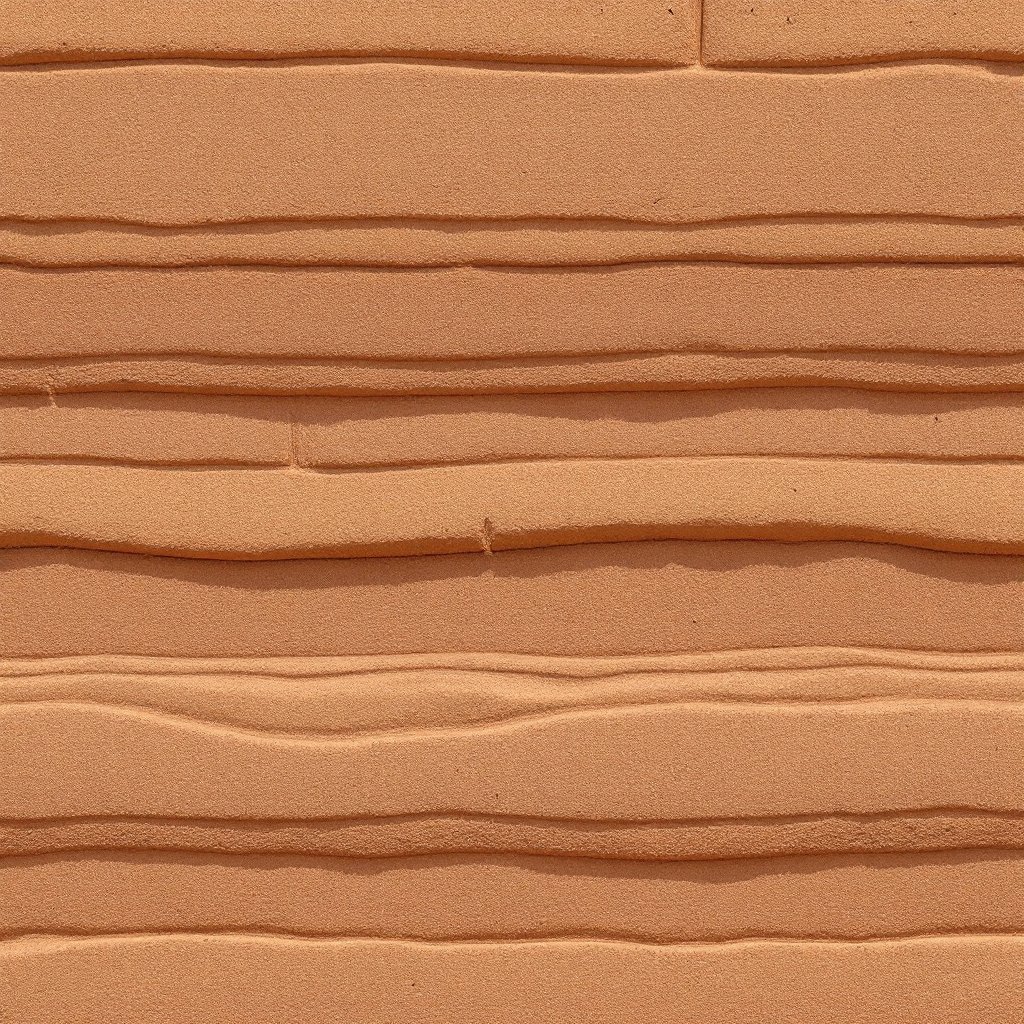

The honest reason: the walls are the most photogenic surface in contemporary architecture. Wineries figured this out first — a stratified wall is a brand asset that pours light across itself twice a day. Estates followed. The image economy did the rest.

Our bet with Bighorn is simple: the moment is real, the specialists are scarce, and the states we serve — Arizona's heartland, and the wide-open markets of Tennessee, Kentucky and Indiana — are where the next decade of American earthen architecture gets built. Start with the material, or start with your land.

It's worth being precise about why the carbon argument suddenly has commercial teeth, because for twenty years it didn't. Cement production accounts for roughly 8% of global CO2 emissions — one material, one industrial process, a share of the planetary ledger comparable to entire nations. Every conventional foundation, every architectural concrete feature wall, every polished floor draws against that account. For most of the green-building era this was a fact you could nod at and then ignore, because nobody with a checkbook was auditing it.

That changed when embodied carbon moved from advocacy literature into procurement documents. Family offices now retain advisors who score real assets on emissions the way they score them on cap rates. Corporate campuses and hospitality brands carry published commitments that flow down, contract by contract, to the general contractor and the concrete truck. A brand that has told its shareholders it will cut embodied carbon cannot pour a signature building out of the very material that dominates the category — not without a footnote it doesn't want to write.

Rammed earth answers this cleanly rather than perfectly, and the distinction matters. A stabilized wall still contains cement — typically 5–10% of the mix — so it is not a zero-carbon fantasy, and we don't sell it as one. But the arithmetic is lopsided: the overwhelming bulk of the wall is soil, often from the site or nearby, unfired, unshipped across oceans, and finished the day the forms come off. No drywall, no paint, no cladding, no replacement cycle. When a material amortizes its footprint across centuries instead of decades, the per-year math embarrasses everything else on the spec sheet. Buyers who audit have noticed. That's new.

The fire argument has undergone the same promotion from talking point to line item. A decade of catastrophic Western fire seasons did more than fill news cycles; it rewrote actuarial tables. Carriers have pulled back from entire ZIP codes. Owners of eight-figure properties in the wildland-urban interface have discovered that the constraint on their build is no longer the architect's imagination but the underwriter's appetite.

Into that conversation walks a wall assembly that is mineral from footing to coping. Compacted earth does not burn, does not off-gas, does not feed an ember storm — it is, in the language of the codes, non-combustible, and in the language of a fire, simply not fuel. We are careful about the promise here: we will not tell you your premium drops by a specific number, because carriers price whole assemblies and whole sites, not walls in isolation. What we can say is that in markets where insurability itself is the scarce commodity, a non-combustible envelope changes which conversations you're allowed to have. For a certain kind of client, that alone justifies the material before anyone mentions how it looks.

And it does matter how it looks. The commercial proof arrived by way of the wine industry, which discovered something the rest of luxury architecture is still catching up to: a building can be marketing you only pay for once. A stratified rammed earth wall photographs like geology — layered, warm, impossible to confuse with anything from a catalog — and a tasting room built from one becomes the most-shared image the brand owns, year after year, without a media budget. Architects noticed which projects kept circulating. Then their residential clients started arriving with the same photographs.

Call it the winery effect: hard evidence that this surface converts attention into pilgrimage. The image economy is fickle about styles but loyal to textures it can't fake, and strata is stubbornly resistant to imitation — printed panels and stained concrete read as counterfeit from across the room. In an era when every finish can be simulated, the unfakeable appreciates.

An honest essay about a rising market names what's pushing back, so here is the other column. First, specialist scarcity: the number of American crews who can execute these walls to a standard we'd put our name on is small, and the craft cannot be hired off a job board or learned from a weekend course. Second, cost: turnkey rammed earth homes run $250–$450+ per square foot, walls alone $50–$225 per square foot of face, and our residential commissions start at $1M. Third, patience: real builds run 16–26 months, and the material rewards none of the shortcuts that compress conventional schedules. None of this is going away soon.

Here's the uncomfortable, honest observation: those frictions are part of why the moment is durable. Materials that scale fast commoditize fast — reclaimed timber went from rare to subscription-box in a decade, and its signal value went with it. Rammed earth's constraints throttle supply at exactly the moment demand is compounding, which means the walls keep signifying what buyers want them to signify: patience, permanence, and the means to commission both. The scarcity isn't a bug in the market. For the people commissioning at this level, it's most of the point.

Forecasting is cheap, so we'll keep ours falsifiable. We expect codes to keep normalizing the material — the engineering precedents exist, the testing protocols exist, and jurisdictions that see one well-documented project approve the second one faster. We expect the crew shortage to ease slowly and unevenly, with quality problems from improvisers along the way; the vetting interview we published elsewhere in this Journal will, regrettably, stay relevant. We expect regional character to emerge the way it always has in earthen building — Arizona's iron-oxide palette reading nothing like the soils of Tennessee, Kentucky or Indiana — so that a decade from now you'll be able to guess a wall's home state from a photograph.

Most of all we expect the fundamental drivers to keep converging rather than fading, because none of them is a fashion. Carbon accounting is regulatory gravity. Fire is climate. The hunger for the singular is as old as luxury itself. When three independent forces push the same direction for a decade, that isn't a trend; it's a correction — the American market remembering a material it had for two centuries and misplaced for one. We built Bighorn to be standing exactly here when it did.

If you're reading this with a parcel in mind, the practical takeaway is simpler than the market analysis: the drivers are working in your favor, the specialists are the bottleneck, and the sensible first move is a conversation about your specific ground rather than more essays. We publish the essays anyway. An informed client is the only kind we want.